Featured

Table of Contents

Monetary specialists suggest keeping the ratio the percentage of total available credit you're using listed below 30%. More from U.S. News initially appeared on Update 01/13/26: The story was formerly released at an earlier date and has been updated with brand-new details.

I want to be upfront about what this page is and isn't. I'm not an investment advisor, and I'm not rendering a verdict on National Foundation for Financial Obligation Management.

Whatever you want to share must be published in the comments by you, with your name connected.

The most valuable thing on this page may not be what I've composed it's the remarks area listed below. People who've actually dealt with National Structure for Financial obligation Management share their experiences there. I 'd encourage you to read them and add your own. An educated consumer is our finest consumer. Sy SymsNational Structure for Financial Obligation Management, Inc.

Instead of repeat what they say about themselves here, I 'd encourage you to read their own website and IRS Form 990 that way you're seeing it directly from main sources, not filtered through me. Before anything else, verify they have the qualifications they claim. Here's what to check for a not-for-profit credit counseling company: The NFCC member directory site lists accredited nonprofit credit counselors.

The Council on Accreditation sets requirements for nonprofit human service companies. Check whether they hold COA accreditation. Check their Bbb profile look at the rating, years in company, and particularly the complaint history and how they reacted. Financial obligation management business must be accredited in each state they run in.

A high BBB grade does not necessarily indicate a company is best for you it indicates they react to complaints filed through the BBB. Read the actual grievance text and the business's responses. That's the beneficial part. See my full guide to what BBB letter grades really suggest The Customer Financial Protection Bureau maintains a public database of problems filed against monetary companies.

Ways to Identify a Leading Certified Financial CounselingWhen you're reading grievances, search for: What the problems have to do with costs, program efficiency, interaction issues? How the company reacted did they fix concerns or simply close them? Whether the exact same concern appears repeatedly a pattern matters more than a single complaintThe ratio of problems to customers a big company will have more problems in raw numbers You can find National Structure for Debt Management on Trustpilot here.

If they're applauding a friendly phone call or easy signup that's interaction quality, not program performance. Compare those against reviews that particularly point out outcomes: financial obligation reduced, program completed, charges as guaranteed. Check out the 2- and 3-star evaluations carefully these tend to be the most sincere, from people who had blended experiences and aren't attempting to tear the business apartLook at how the company reacts to unfavorable reviews a protective or dismissive action tells you somethingCheck the evaluation dates a flood of 5-star evaluations in a brief period can show a solicitation campaign1-StarRead These First They Reveal Patterns5-StarLook for Specific Outcomes Not Simply Applaud As a not-for-profit, National Foundation for Financial obligation Management is required to submit an internal revenue service Type 990 every year and those filings are public.

Essential Debt Tools for Accurate 2026 Planning

When you open a 990, here's what to search for: What does the CEO make? Is it proportionate to the organization's size and mission? Are they running surpluses or constant deficits? Numerous deficit years can signify monetary instability. How much of their earnings originates from the charges customers pay versus grants and contributions? Read their description of program services.

Credit counseling firms likewise earn "fair share" payments from creditors when clients enroll in financial obligation management plans. The 990 is your window into how they really operate.

Verify credentials through NFCC, COA, BBB, and NMLS before anything elseSearch the CFPB grievance database for patterns not simply raw numbersOn Trustpilot, compare 5-star reviews about interactions vs.

National Foundation for Structure ManagementFinancial Obligation Inc. is registered as signed up 501(c)( 3) nonprofit organization not-for-profit company IRS under EIN 59-3556825. Their yearly Type 990 filings are available to the public through ProPublica's Nonprofit Explorer. You can also file with your state lawyer general's office and the BBB.

Handling Loan Balances Plans in 2026

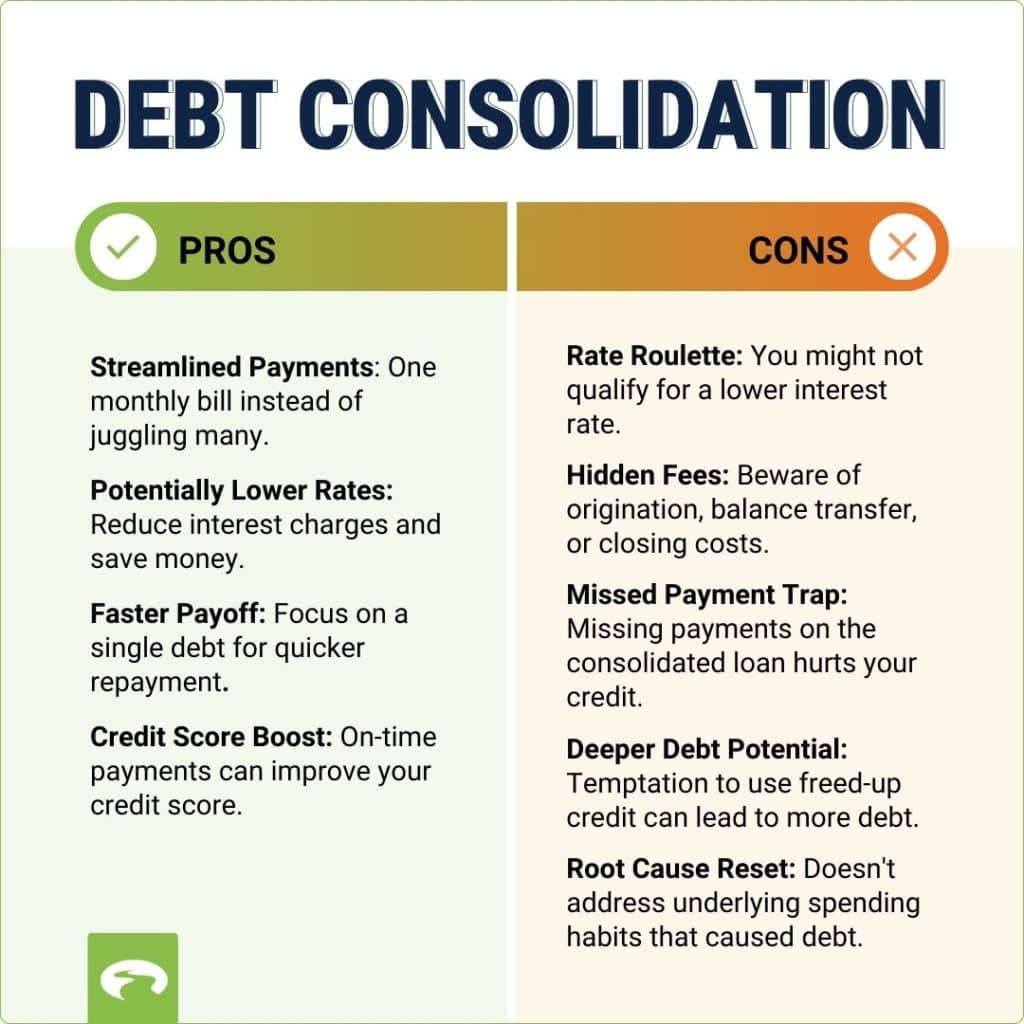

I 'd motivate you to inspect that straight in the NFCC member directory site and on the COA site accreditation status can alter, and you'll want to validate the present status from the source rather than take my word for it. A financial obligation management plan (DMP) is a structured repayment program where a credit counseling firm works out with your lenders to potentially decrease your rate of interest.

DMPs usually take three to five years to complete and require consistent month-to-month payments. They're not the best fit for every situation.

Your viewpoint assists others make a more educated choice. Scroll to the bottom of this page the remarks box exists. + Free Newsletter Your Cash Actually The unfiltered debt takes I can't fit on this website for people making great money who are still drowning in financial obligation. + Customer debt expert & investigative writer.

Washington Post award-winning author. Exposing financial obligation scams given that 1994.

Rising monetary pressure is driving need for financial obligation options, and National Debt Relief uses a tested, widely available path towards debt resolution. Charge card balances in the United States climbed up past $1.2 trillion in 2025, with typical rates of interest topping 22%. For many households, making minimum payments every month hardly dents the balance.

Navigating Debtor Education Steps in 2026

Versus this backdrop, more borrowers are turning to debt settlement business for relief. These programs negotiate with lenders to lower the overall amount owed on unsecured financial obligations like charge card, medical costs, or individual loans. While financial obligation settlement is not the best fit for everyone, it has actually ended up being a recognized choice for people with significant unsecured debt who wish to explore options to bankruptcy.National Financial obligation Relief is among the most widely known companies in this area. The business deals with thousands of financial institutionsacross the country and fixes tens of countless debt accounts monthly. Because introducing, it has assisted settle millions of private debts for customers throughout the country. Reputation and oversight also matter when comparing debt relief business. National Financial Obligation Relief is a recognized member of the Association for Consumer Debt Relief (ACDR ), which sets requirements for ethical practices in the debt settlement market. Third-party recognition has also strengthened its track record. In 2025, Forbes Advisorranked National Financial obligation Relief as the very best debt settlement business, citing its transparency and broad accessibility. When comparing the leading debt relief companies, the structure of the program matters. National Debt Relief utilizes a financial obligation settlement technique, which varies from choices like financial obligation combination loans or credit counseling plans that focus on interest rate reductions or extended repayment terms. They transfer funds every month into a dedicated account in their own name. Those funds are later on utilized to resolve debts through worked out settlements. National Financial obligation Relief handles lender settlements on behalf of customers once enough funds are readily available, while clients retain the capability to examine and approve each proposed settlement before it is finalized. For numerous customers, programs are developed to take between 12 and 48 months. This range is constant with other large, established financial obligation relief companies.

{kind=link}

Latest Posts

Securing Low Interest Personal Loans in 2026

HUD-Approved Property Education in 2026

Top Credit Management FAQs for 2026